| work-on-the-boards Firms Report Steady Growth in October Most expect design upturn to continue through 2007 Summary: Design activity for nonresidential buildings remained strong in October, while residential activity continued its downward spiral. Overall, the AIA’s Architecture Billings Index just about maintained its September level. Firms are expecting modest gains in activity next year, with larger firms the most optimistic.

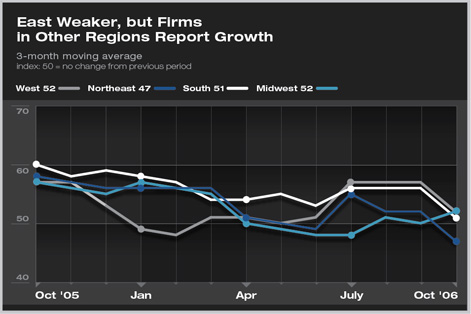

Regional readings were unusually volatile in October. Firms in the Midwest had been reporting weakening conditions in recent months; however, the October score rebounded to its strongest pace of growth since the first quarter of the year. Firms in the South and West reported continued growth, but the pace of growth was down from recent months. Finally, firms in the Northeast reported only their second decline in billings since late 2003. The continued weakness in the residential sector is a key reason for those firms that reported softening business conditions in October. Both the commercial/industrial and institutional sectors remain strong. Commercial/industrial firms and institutional firms each reported healthy gains in billing for the month: the ABI for commercial/institutional firms was 55.7 for October, while running 52.3 for institutional firms. Both scores were below their September readings.

Overall economy growing, but slowly One positive coming from the recent softening in overall economic activity is the easing in inflation. Helped by the recent drop in oil prices, the annual increase in consumer prices was running at just over 2 percent in September, down from over 4 percent as recently as last July. Wholesale prices likewise have been dropping recently. Easing in producer (wholesale) prices should help rein in some of the jumps in construction products that have plagued the industry in recent years.

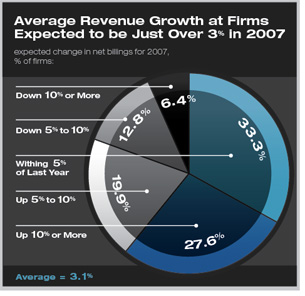

Regionally, firms in the South are expecting the strongest growth next year, averaging between 4 percent and 5 percent, while Midwestern firms have the lowest expectations for their revenue growth next year. Firms in the West are more optimistic than their counterparts in the Northeast. Firms with annual revenue of $5 million or more are the most optimistic, expecting revenue growth of about 7 percent next year. Almost two-thirds of firms of this size expect growth of 5 percent or more next year, while fewer than 5 percent expect declines of that magnitude. Firms with annual revenue of under $1 million expect almost no growth next year on average, while firms in the $1 million to $5 million category expect revenue growth averaging about 5 percent. The low expectations for next year for smaller firms are in large part due to the weakness in the residential sector. Residential firms (where more than half of their revenue comes from residential projects) are expecting no gains in revenue next year on average. Commercial/industrial firms are the most optimistic, with expected growth averaging more than 5 percent. However, institutional firms are also upbeat about their prospects for 2006, expecting growth just below 5 percent on average. |

||

Copyright 2006 The American Institute of Architects. All rights reserved. Home Page |

||

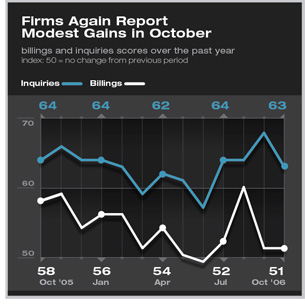

Architecture firms reported a modest overall increase in billings in October, with the AIA’s Architecture Billings Index recording a score of 51.2 for the month, down slightly from the 51.4 reading in September. Any score above 50 indicates that billings are increasing nationally. Inquiries for new projects remained strong with a score of 62.7, however the inquiries index fell from its unusually strong 67.7 reading in September.

Architecture firms reported a modest overall increase in billings in October, with the AIA’s Architecture Billings Index recording a score of 51.2 for the month, down slightly from the 51.4 reading in September. Any score above 50 indicates that billings are increasing nationally. Inquiries for new projects remained strong with a score of 62.7, however the inquiries index fell from its unusually strong 67.7 reading in September.

Expectations for 2007 highest in the South

Expectations for 2007 highest in the Southnews headlines

practice

business

design

Recent Related

› September’s Billings Up Modestly; Inquiries Much Stronger

› Firms Enjoy a Late Summer Surge

› Business Conditions at Architecture Firms Improve in July

› Weakness in Residential Sector Causes Firm Billings to Fall Again in June

› Business Levels Decline in May After Several Months of Softening

This month, Work-on-the-Boards participants are saying:

Activity seems very strong; the housing market slowdown has not greatly affected the public sector markets in which we work.

—75-person firm in the Midwest, institutional specialization

State review of hospitals has slowed up construction in that market.

—45-person firm in the Northeast, institutional specialization

We experienced lots of interest in commencing projects through the summer. Many leads are real, but for various reasons the projects are struggling to get started.

—23-person firm in the West, mixed specialization

Business is so strong that the labor pool of qualified talent is terribly thin.

—11-person firm in the South, commercial/industrial specialization.

A

printer-friendly version of this article is available.

Download the PDF file.